One API over a network of licensed payment partners: hosted KYC, virtual accounts, and payouts to 130+ countries, settled on stablecoin rails. No float to fund, no keys to hold.

Production-deployedSandbox self-serve todayLive-money mode switches on per agreement

POST /v1/transfers

{

"customer_id": "cus_8f21",

"quote_id": "qt_e930",

"beneficiary_id": "ben_1d47"

}

201 Created · status: processingevent: transfer.settled ✓

Transfercompleted

$1,000.00

to NGN · Nigeria · arrived in 9m 41s

Chinedu OkaforZenith Bank ••4821~10 min

Price locked at quote. No surprises at delivery.

SEPAFaster PaymentsPixSPEIACHIMPSZenginGCash+ 12 more on bank transfer and mobile wallet · SWIFT for everywhere beyond

Public API

Callable now · no key needed

130+ countries

Bank transfer · mobile wallet

20 published corridors

15 active · Pix, SEPA, SPEI, ACH and more

Self-custody

BYO wallet · no keys held

01

Global money movement should not take five vendors and a year.

Fintechs, payroll platforms, marketplaces, developers and wallets all hit the same wall: onboarding, accounts and payouts that land locally, rebuilt vendor by vendor, market by market. Stablecoins already won settlement (~$9T adjusted volume in 12 months, a16z 2025), yet real-world payments are only $390B (McKinsey / Artemis). The gap is the fiat last mile.

The stitched stack

Every team that moves money stitches together a network of PSPs, a verification vendor, a payout provider per region, plus the licensing and treasury to hold it up.

The corridor tax

Local licensing, bank-form quirks, sanctions screening and payout partners turn one corridor into a quarters-long project before the first dollar lands.

The vanishing vendors

Bridge into Stripe, Fern into Rain. Each deal takes an integrator-first vendor off the market and leaves its integrators re-platforming.

Stablecoin settlement is solved. Getting money into a bank account in Lagos, Manila, or Mexico City is not.

six vendor systems → one API · one agreement

02

The category just got priced, and the neutral vendors keep disappearing.

B2B stablecoin payments are now the largest real-world stablecoin segment (McKinsey / Artemis), while a wave of acquisitions keeps removing the independent, integrator-first vendors. The market is priced, and the neutral slot keeps re-opening.

733%

B2B stablecoin payments growth in 2025, year over year

mckinsey · artemis · 2025

$226B of $390B

Now the largest real-world stablecoin payment segment

real-world stablecoin payments

60%

Share of all real-world stablecoin payments that is B2B

the category is priced · growing

consolidation.log

tail -f consolidation.log

2025-02 bridge → stripe $1.1Bclosed · off the market2025-05 conduit raises $36Mseries A on $10B+ volume · independent2025-12 fern → rain absorbedoff the market2026-03 bvnk → mastercard $1.8Bannounced · pending close// every exit validates the price of the layerslot: neutral, integrator-first payout API → re-opening

Deal figures as announced: Stripe closed Bridge Feb 2025; Rain absorbed Fern Dec 2025 and went on to raise $250M; Mastercard announced BVNK Mar 2026; Conduit's Series A per its own post, May 2025.

03

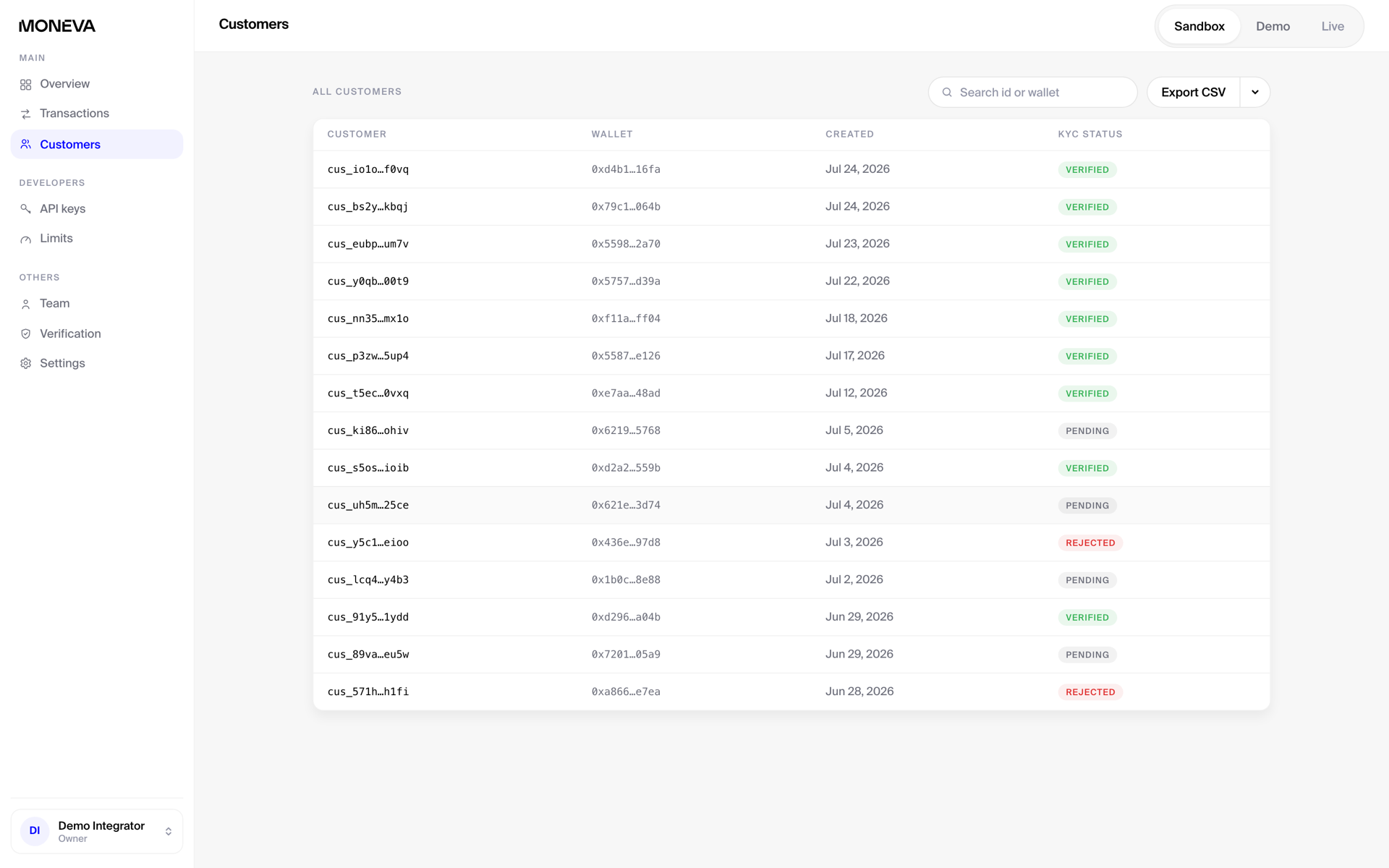

KYC, virtual accounts and payouts, behind one API key.

Moneva Platform is one API over a network of licensed payment partners: hosted KYC, named virtual fiat accounts, payouts, compliance and monitoring. The working promise, verbatim from our docs: onboard a user, issue their account, and move money in and out, in one afternoon, against a self-serve sandbox.

Live corridor endpoint: mid-market rate, fee-derived minimums, estimated arrival. Speeds from minutes (MXN) to 1 to 3 business days (USD ACH).

Virtual accounts · named details per customer

Account detailsUSDEURGBPNGN

Account holderADA OKAFOR

Account number8331 2076 4409

Routing number · ACH026 073 150

IBAN · EURDE89 3704 0044 0532 0130 00

Sort code · GBP23-14-70

Account number · NGN3082 4115 79

Named USD, EUR, GBP and NGN account details per customer, issued through licensed partners. Every deposit settles as stablecoin in the customer's own wallet. Details illustrative.

Where we are aheadA partner network, not one vendor · corridors are added, not re-contracted15 active corridors · vs Bridge 8 rails, Conduit 5Virtual accounts in USD, EUR, GBP and NGN · vs BVNK EUR-onlyYou do not need your own licence · BVNK requires oneNo pre-funded float · six of seven majors require it

Own object model

Customers, accounts, quotes, beneficiaries, transfers, events. Signed webhooks with a durable, replayable event log. First-class test mode.

Forms as API

Beneficiary bank forms served as schemas per corridor. Integrators render fields from the schema and never guess a bank form again.

A network, not a single vendor

Licensed PSP and payout partners provide the regulated rails, KYC, and local payouts. Moneva is the single API, object model, and compliance layer over the whole network.

04

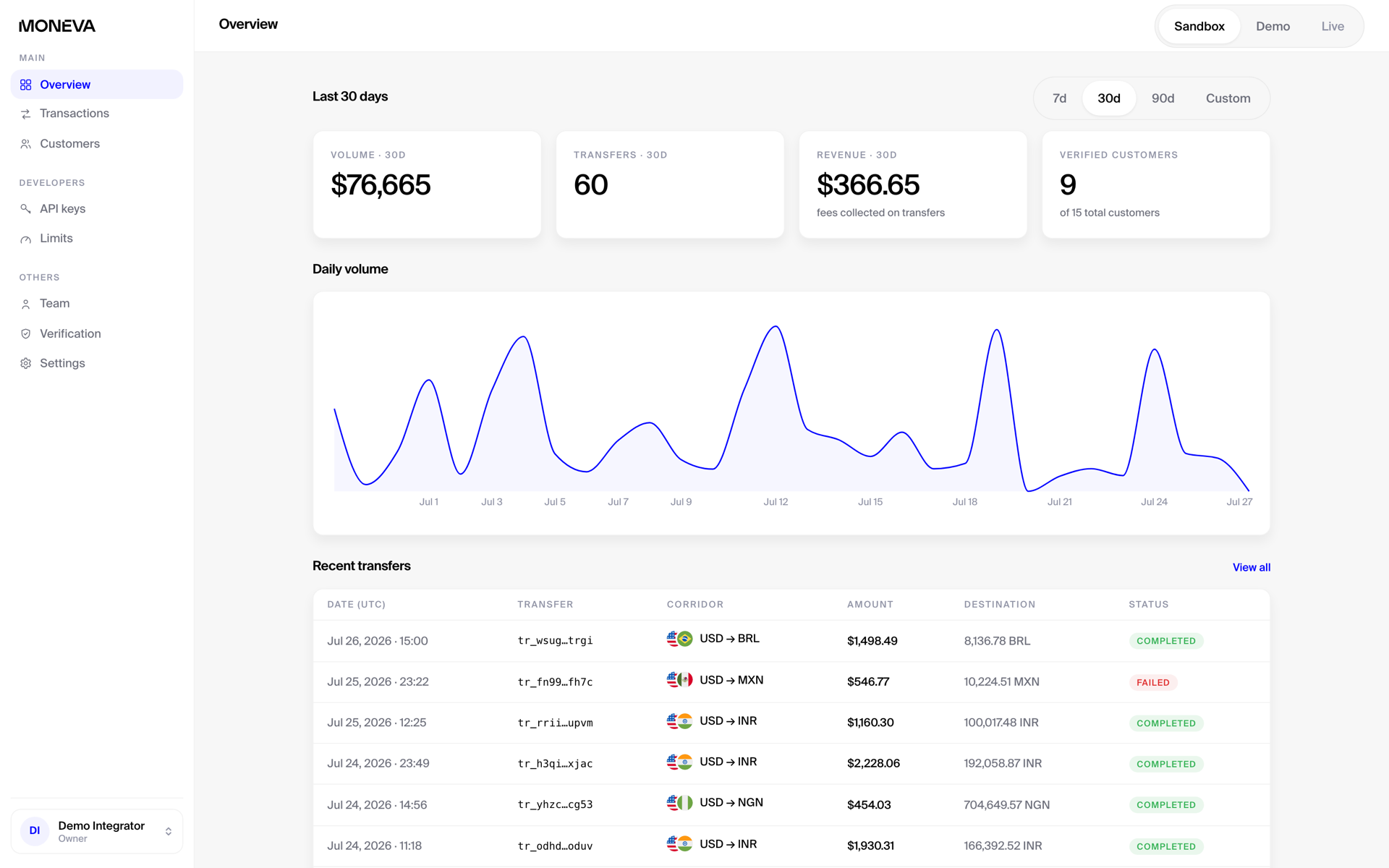

Payouts to 130+ countries, on local rails or SWIFT.

One integration reaches 130+ countries through the network of licensed payment partners. The 20 published corridors, 15 active are the deepest rails: local currencies, local bank systems, minutes-fast settlement, with more in the pipeline.

130+ countries · payout coverageNot yet covered

20 published corridors, 15 active · local bank rails and currencies

USDEURGBPMXNBRLARSNGNKESGHSEGPINRPHPVNDIDRPKRTRYJPYAEDOMRQARNext in the pipelineGTQCOPSGDCAD

Bank transfer

Local rails: SPEI, Pix, SEPA, NIBSS and more. Minutes-fast on the deepest corridors, plus SWIFT reach.

Mobile wallet

Mobile money payouts, M-Pesa-style wallets across Africa and Asia, delivered like any bank payout.

Near mid-market FX. Speed examples illustrative; live per corridor from /v1/corridors.

05

Your users, your wallets, our rails.

BYO wallet: EOA, smart account, or MPC, from any vendor. Ownership is proven by wallet signature, EIP-4361 for EOAs and ERC-1271 for contract wallets, or by a one-time code on the licensed rail for non-EVM users: both open the same six-day session. No wallet migration, no SDK lock-in. TypeScript SDK and React hooks in beta; the integrator dashboard handles keys, team, usage, and exports.

Sandbox to settled payout · six steps

transfer flow keys never leave the wallet

Integrator app

Moneva Platform

Licensed PSP rails

On-chain

1

Create customer

Integrator calls the API; hosted KYC handles onboarding.

kyc

2

Prove the wallet

Wallet signature (EIP-4361, ERC-1271), or a one-time code for non-EVM users.

signature · otp

3

Quote locked

Mid-market rate with transparent fee lines.

quote

4

Stablecoin funds it

Transfer funds on-chain from the user's own wallet.

settle

5

Fiat lands

A licensed PSP partner pays out local fiat in the corridor.

payout

6

Webhook fires

transfer.settled hits the integrator app; event log is replayable.

event

create customer→prove wallet→quote→settle→webhook

The same lane diagram is the integration guide in our docs. Any wallet vendor, any architecture; nothing to migrate.

06

Remittance rails still cost 6.36% on average.

Costs are World Bank Remittance Prices Worldwide, Issue 54 (Q3 2025). The stablecoin leg costs cents, settles in under a minute, and runs 24/7. Moneva all-in is illustrative, per the pricing model.

Banks as sending providerMost expensive provider type, $200 send

Banks

14.99%

Sub-Saharan Africa corridorsMost expensive receiving region

SSA

8.46%

Global averageAll providers, $200 send

Global

6.36%

Moneva all-inillustrative, per pricing model

Moneva

0.3% to 1.0%

legacy rails 6% to 15%→stablecoin rails <1%→the spread is the revenue pool

The spread between legacy rails and stablecoin rails is the revenue pool. We sell it as an API.

07

No float to fund, and no keys to hold.

Traditional payout networks make every partner pre-fund the destination: nostro accounts, float parked per corridor, FX inventory. On Moneva, every transfer is funded just in time from the end customer's own wallet, settles on stablecoin rails, and licensed partners pay out local fiat from their own liquidity. The integrator brings neither float nor FX inventory. Nothing is pre-funded, nothing is parked.

×What integrators never bring

×Pre-funded float per corridor

×Nostro / settlement accounts

×FX inventory and rebalancing desks

×Banking relationships in each country

×Liquidity or treasury ops headcount

✓What they get

✓Just-in-time funding from the customer's own wallet, per transfer

✓Licensed partner liquidity pays out the local fiat leg, in 15 active corridors

✓Payouts to 130+ countries by bank transfer or mobile wallet

✓Fees settled atomically inside the transfer

✓One agreement, one API, one compliance posture

wire the float→it sits idle→rebalance forever

Thunes calls pre-funding “millions of dollars in trapped working capital”. That is their own description of the model we removed.

08

Not a roadmap. Call it right now.

The platform is production-deployed and running today: API, docs, and integrator dashboard, monitored around the clock. Integrations run in sandbox while the first commercial agreements are signed; live-money mode is already built and switches on per agreement. Not an engineering milestone, a signature.

Live nowAPI · docs.moneva.ioSelf-serve docsIntegrator dashboardLive corridor data · publicSandbox + test mode · self-serveLive-money mode built · switches on per agreement

dashboard.moneva.io

Corridors & compliance

Corridor data, fail-closed screening

Full beneficiary schemas, live rates, and estimated arrival per corridor. OFAC wallet screening at customer create, fail-closed. Purpose-of-payment enforcement on regulated corridors.

Ops maturity

Run like production, because it is

Continuous verification against the live rail caught a half-wired corridor in July, before any integrator could. Monitored around the clock, with strict compatibility guarantees on the API contract.

Dashboard

Self-serve integrator console

Passwordless auth, transactions and customer detail, reveal-once API keys, team invites, CSV/HTML/PDF exports with QR statement verification and a public verify page.

09

We were our own first customer.

A full consumer neobank app built on these exact rails: iOS on TestFlight (build 17), Google Play submission in review, real mainnet transactions in the sandbox, end to end. Every hard part of the platform exists because we hit it in production first.

Accounts

Local account details

USD, EUR, GBP, and NGN account details, issued through the platform.

Remittances

Payouts to 130+ countries

Lands in ~10 minutes, near mid-market, on licensed partner rails.

QR Pay

Scan to pay locally

QR payments settled in stablecoins across Latin America.

Receive

Virtual fiat accounts

USD, EUR, GBP and NGN account details from the platform's account objects.

Send

Payouts to 130+ countries

~10 minutes, near mid-market, on licensed partner rails; the platform's corridors carry the deepest flows.

Hold

Multi-chain wallet

One balance view across chains, funded by real mainnet transactions.

Prove

Verifiable statements

SHA-256 hashed, dual-signed EIP-712; anyone can verify authenticity.

Built on the same public API an integrator uses, so the platform is proven by a real product, not a demo.

10

Retail is 3% of cross-border flows and 43% of the revenue.

We take a software rake on the fastest-converting flow in payments. Sources: FXC Intelligence 2025, McKinsey, Artemis.

Cross-border payments revenue pool

$316B

$178.8T of cross-border flows at a 0.18% blended margin. McKinsey Cross-Border Payments Map, April 2025.

▾

Retail cross-border, where the margin actually is

$136B

C2B $69B, P2P $42B, B2C $25B. About 3% of flows and 43% of revenue, at 1.3% to 3.4% margins against 0.1% on wholesale B2B.

▾

Our wedge: integrators paying out on these rails

Bottom-up

Priced per integrator from the pricing model, not as a share of the pool.

97% of flows are wholesale→0.1% margin→retail is 3% of flows, 43% of revenue

We sell into the thin, high-margin slice, not the fat one.

11

Land integrators where the corridors are already running.

Self-serve sandbox to signed agreement: the one-afternoon integration is the acquisition funnel. The consumer app doubles as reference implementation and public demo.

Fintechs & neobanks

Global payin and payout rails without licensing them: one agreement instead of a vendor per market, virtual accounts in USD, EUR, GBP and NGN.

POST /v1/customers

Developers & product teams

Accounts, deposits and payouts behind one key. The first corridor call is public, and the first integration takes an afternoon in the sandbox.

GET /v1/corridors

Wallets & crypto platforms

A compliant fiat last mile for stablecoin balances. BYO wallet, no migration, no SDK lock-in, and their own fee line on every payout.

POST /v1/…/wallet_sessions

Payroll, contractor & remittance apps

LatAm and Africa corridors on local rails, minutes-fast on MXN, BRL, NGN and ARS. Purpose-of-payment handled on regulated corridors.

POST /v1/transfers

Marketplaces & platforms

Pay out to a bank account or mobile wallet. Beneficiary schemas per corridor, machine-readable; signed webhooks and a replayable event log.

GET /v1/…/beneficiary_schema

Anyone else: scope it with us

Tell us what you are moving and we scope it against the active corridor set. Sandbox access the same day.

Corridor-led expansion: launch where the active corridors overlap integrator demand. GTQ, COP, SGD, and CAD are next in the pipeline.

12

Committed minimums plus usage, collected on-chain.

Three illustrative tiers, negotiated per agreement on a 1- or 2-year retainer: a committed monthly minimum with included volume, where a 2-year term buys better pricing. No integration or setup fees; the integrator’s all-in lands between roughly 0.3% and 1.0% at typical ticket sizes, with a $0.50 minimum and a $250 maximum per transfer. These are Moneva’s platform fees to the integrator, not the end-customer price: the integrator sets their own fee line on top and keeps it. Fees are legs inside the transfer itself: paid the instant money moves, atomic with settlement. Zero billing infrastructure, no receivables, no integrator credit risk.

Starter

$1,000/mo minimum

Included volume$100K/mo~100 bps implied

Overage60 to 90 bps0.6% to 0.9%

Per-transfer minimum$0.50whichever is greater

Target integratorPilot fintechs and wallets launching a first corridor, under $150K/mo flow.

Growth

$2,000/mo minimum

Included volume$250K/mo~80 bps implied

Overage · first $10K0.70%of each transfer

Overage · above $10K0.20%marginal, per slice

Per transfer$0.50 min · $250 maxfees never exceed $250

Target integratorLive consumer fintech or payroll platform, $0.2M to $1.5M/mo.

Scale

Custom · per agreement

CommitmentPer agreement2-year terms buy the best rates

ScheduleNegotiatedcustom breaks and rates

Per-transfer minimum$0.50whichever is greater

Target integratorRemittance apps, neobanks, and exchanges above $1.5M/mo.

Unit economics

~68% gross margin

Illustrative Growth integrator, $500K/mo over 500 transfers: $2,000 minimum + $1,750 metered ($7 per $1,000 transfer at 0.70%) = $3,750/mo revenue. The licensed rail prices per transfer, not per dollar: about $1.2K at this mix, and margin rises with ticket size. Integrator all-in: 75 bps vs 300 to 800 bps legacy.

Why it holdsInside the published infra band (Stripe payouts 25 to 125 bps, Nium 30 to 80 bps, Wise ~50 bps blended) because it bundles KYC, virtual accounts, and licensed corridor access.

What’s included, in every tier

✓Hosted KYC & KYB✓Virtual accounts · USD, EUR, GBP, NGN✓Payouts to 130+ countries✓Your own fee line on every transfer✓Sanctions & wallet screening✓Signed webhooks · replayable event log✓Dashboard, team & exports✓Self-serve sandbox & docs✓SWIFT beyond local rails✓BYO-wallet self-custody

No gated features, no add-ons. Tiers change price, never capability.

Why this spread is reasonable: at 0.3% to 1.0% all-in, the integrator keeps most of the 3% to 8% the legacy rails used to take, and the fee buys the licensed rail, hosted KYC and compliance they no longer build. Every overage is negotiated inside that band; the pricing goal is that the integrator makes money on every corridor, because the model only works when they win.

CommercialsNo integration or setup feesProgressive pricing · bigger transfers, lower ratesMoneva’s fee to the integrator · their own fee line on top1-year standard · 2-year preferred ratesMonthly minimum + included volume over the committed term

All figures illustrative. Tier numbers and overage bps are negotiated per agreement; comparables per cited research, vendor-published or third-party estimates as labeled in the pricing model. The overage fee is a fee leg inside the transfer, so Moneva is paid the instant money moves.

13

No setup fees, no shared take: the model is built to compound.

Adjacent models monetize the same flows with worse economics. Card platforms keep a slice of interchange that is split with the network and the sponsor bank and capped by regulation in Europe; banking-as-a-service sells implementation projects and rate-dependent float. Moneva charges on movement: nothing up front, a fee shared with nobody, flat per-transfer costs underneath.

Card-issuing platforms

Interchange: shared and capped

Cost to startFive figuressetup, card fees, reserves

Take~15 to 30 bpsnet of card spend · public filings

CarriesFraud + disputesEU interchange capped at 0.2% to 0.3%

ReachCard-network footprintissuing set up region by region

ServesCard-eligible usersbanked cardholders only

Banking-as-a-service

Implementation and float

Cost to start£15K to six figuresimplementation measured in months

$13 to the integratortheir margin, on every transfer

$0 to start→usage fees, unshared→flat costs underneath

Sustainable on both sides: the integrator starts free and keeps their own fee line; Moneva earns on every dollar moved. No interchange caps, no acquirer roadmap, no float bet.

14

Everyone else makes you fund the float first.

Bridge is inside Stripe, BVNK is joining Mastercard, and Fern was absorbed by Rain: the independent slots are emptying out. Moneva: a $1,000/mo entry floor, roughly 0.3% to 1.0% all-in negotiated per agreement, never more than $250 per transfer, zero integration or setup fees, and the integrator's own fee line as a first-class product feature.

Provider

Pre-fund a fiat balance?

Published entry cost

Time to production

Self-serve sandbox

Payoneer

Required

Rate card only

Not stated

Partial

Nium

Required

Not published

Not stated

Yes

Thunes

Required

Not published

Not stated

None

Rapyd

Required, plus reserve

Cards only

Up to 30 days

Yes

Column

Locked reserve

Not published

Not stated

Yes

Rain (Fern)

Required

Not published

Not stated

Access-code gated

Griffin

n/a

From £15k + £3.5k to £10k/mo

6 to 8 weeks

Yes

Moneva

None. Per-transfer settlement

From $1,000/mo · no setup fee

Sandbox today

Yes

Assessment from each provider’s own public documentation, July 2026 (sources below), except Rain, whose API docs are access-gated and whose pre-funding requirement is from direct market knowledge. Wise Platform is the one documented exception on pre-funding: its bulk settlement extends credit, but only to “select partners”. Integrating Bridge or BVNK means building on an acquirer’s roadmap. Moneva routes over a network of licensed payment partners and stays independent of any one of them.

Only on MonevaBYO-wallet self-custodyOn-chain fee collectionQR-verifiable statementsForms-as-API corridor schemas

15

Every corridor we run makes the next one harder to copy.

The moat is not "we use stablecoins". It is corridor depth, reliability, and a fee mechanism nobody else ships, each getting harder to copy with every corridor we bring up.

Corridor coverage & schema depth

Every beneficiary field, purpose code and bank quirk in the published corridors was learned against live partner rails. Anyone following re-earns it corridor by corridor.

Reliability layer as switching cost

Around-the-clock verification against the live rail, and strict compatibility guarantees on the API contract. Integrators build against behavior that provably does not drift.

On-chain fee collection

Fees settle as legs inside the transfer, atomic with the payout. No invoicing, no receivables, no credit risk. Nobody else ships this.

Verifiable-statement trust layer

QR-verifiable, cryptographically signed statements across platform exports and the consumer app, with a public verify page.

Licensed partner network

Regulated rails, KYC, and payout coverage assembled behind one agreement and compliance posture. Operationally hard to replicate.

The app as living demo

A full consumer neobank running on the same rails is a permanent testbed and the most honest sales demo in the category.

16

Self-custody only, with compliance running the whole lifecycle.

"Integrators bring their own wallets. Moneva never holds keys, never commingles, never takes deposits." We are software on top of licensed rails, with no custodial surface to regulate.

Integrator wallets

Keys stay here

EOA, smart account, or MPC, from any vendor. Ownership proven by wallet signature, EIP-4361 for EOAs and ERC-1271 for smart accounts, or a one-time code for non-EVM users.

Moneva Platform

Software only

Orchestration, corridor schemas, quotes, webhooks, and screening. Moneva never holds keys, never commingles, never takes deposits.

Licensed partners

The regulated surface

Regulated fiat rails, KYC, and payouts sit with licensed ramp and KYC partners. OFAC screening fail-closed at onboarding; purpose-of-payment enforced where corridors require it.

Compliance layer · onboarding to 24/7 monitoring

1

Onboarding KYC

Hosted verification via licensed partners; webhook-driven status, no document handling for the integrator.

customer create

2

Sanctions & wallet screening

OFAC and wallet screening at customer creation. Fail-closed: no clear result, no customer.

fail-closed

3

Corridor compliance data

Purpose of payment and sender-recipient relationship collected and enforced on regulated corridors.

per corridor

4

Ongoing monitoring

Transaction monitoring plus 24/7 automated verification of the rail itself, with alerting.

24/7 · ongoing

17

Nine months, sized to reach the first signed integrators.

The platform is live and our own app is integrated end to end. Capital converts a working product into paying integrators and the repeatable economics that get Moneva to a seed round.

ShippedAPI · 20 published corridors, 15 activeIntegrator dashboardSelf-serve docs24/7 monitored operationsConsumer app on TestFlight

Milestone 01 · Revenue

First paying integrators

First agreements signed; live-money mode switched on

Pilot integrators converted from the sandbox funnel

Committed minimums collected on-chain

Milestone 02 · Depth

Ship what integrators hit

Cross-chain funding and ops console shipped

Corridors expanded per demand: GTQ, COP, SGD, CAD pipeline

SDK and React hooks out of beta

Milestone 03 · Seed-ready

Repeatable integrator economics

Volume and revenue per integrator cohort

Gross margin holding near the ~68% model

Seed raise on proven unit economics

The core build is done. This round funds corridor depth, reliability and the first integrations, not a rewrite. Nine months at a founder-led burn, sized to reach signed integrators and the volume that opens a seed.

18

We are raising a round to win the first integrators.

Backing a technical founder who has shipped on-chain financial infrastructure, operated inside banking and fintech, raised capital, and built the live platform end to end, with a co-founder running partnerships and operations.

Chester Bella

Founder & Product Developer · Moneva

Ex-N26, banking operations; Product Owner at Europace, Germany's largest mortgage platform

Hands-on founder, building Moneva end to end

Danny Boahen

Co-founder & Business Operations · Moneva

Ex-N26, banking operations; ex-Interhyp, Germany's largest residential mortgage broker

Owns business operations: partnerships, integrator pipeline and commercial ops

TogetherUniversity classmatesETHDenver speakersMultiple ecosystem grantsBuilt a DeFi perps protocol · ~$267K community raisearXiv whitepaper co-authors ↗

Raising

$250K

Post-money SAFE · $10M cap · 2.5% to investors · ~9 months at a ~$28K monthly burn

USD

USD EUR

EUR GBP

GBP MXN

MXN BRL

BRL ARS

ARS KES

KES GHS

GHS EGP

EGP INR

INR PHP

PHP VND

VND IDR

IDR PKR

PKR TRY

TRY JPY

JPY AED

AED OMR

OMR QAR

QAR GTQ

GTQ COP

COP SGD

SGD CAD

CAD Chinedu OkaforZenith Bank ••4821~10 min

Chinedu OkaforZenith Bank ••4821~10 min

Payoneer

Payoneer Nium

Nium Thunes

Thunes Rapyd

Rapyd Column

Column Rain (Fern)

Rain (Fern) Griffin

Griffin Moneva

Moneva